This company will self-destruct after its ICO

Investors and entrepreneurs are moving into a world where token networks influence the way new businesses are established and run. This is a sea change, a complete rethinking of the startup model for network businesses, and if businesses aren’t ready, they will be left behind.

Network businesses — especially the ones that are harder to grow and monetize and have historically used advertising — uniquely benefit from being implemented as token networks rather than companies servicing customers. “Token Networks” change the way we think about startups from a company where customers pay for a service to a token-accessible network where you plan, engineer and maintain an economy. Value created in a token-based economy can be more efficiently shared between the different token holders: founders, builders, customers, service-providers and investors.

And yet, recent weeks show strong headwinds for ICOs.

Two opposing fears are holding back the move to token-networks: a fear of the absence of governance on one side and a fear of regulation on the other.

There is, however, a solution to both of these contradictory concerns when it comes to company creation in the token era.

Burn it all down. Create a self-destructing company which would start off as a traditional company with equity investment but at some point discard its “corporate shell” and switch to a decentralized network governance structure.

Part of the problem is that the rulebook governing token-network formation and fund-raising is still being invented & written. In 2017 we saw projects raise what’s comparable to hundreds of millions of dollars via Initial Coin Offerings (ICOs), using little more than a picture of a few smiling founders and an impenetrable white paper.

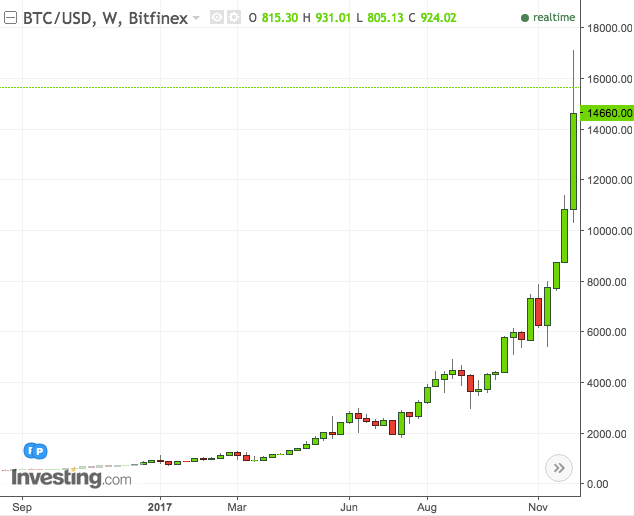

The key driver for the fundraising success of many of the ICOs is the availability of “free money” thanks to crypto-angels born through one of the fastest waves of wealth creations in modern history. If you tracked bitcoin, ethereum and other crypto-currencies any time in the past decade you saw over $500 billion created in less than 10 years, $450 billion of which appeared in the past year alone (As of December, 22, 2017).

Tracking bitcoin’s remarkable rise

The sheer amount of money flowing into the market allowed early ICOs to have no governance structure whatsoever. Like in any nascent field, there are scams and scammers. Penny-stock IPOs have gone through a similar process before, instigating heavy regulatory counter-action in the 1930s which birted the requirement for companies to have tens of millions in revenue in order to go public. History doesn’t repeat itself, but it rhymes. ICOs are going through a similar process today.

Moreover, the SEC, as a primary regulator of securities, has provided an investigative report about one of the first ICOs: the DAO. The focus of the investigative report was the principal/agent problem: having governance by a small group of managers with divergent interests is the primary reason that the SEC needs to be involved. This is driving a fear of regulatory intervention, and as expected, the SEC has cracked down on multiple ICOs recently.

Because regulators are now involved, legal firms have been giving quotes in the hundreds of thousands of dollars for representing companies that intend to ICO. At the same time, the risk appetite by funders previously happy to fund teams & ideas has waned and now they prefer to fund more mature projects; ones that already have built out the token network. In short, it’s getting harder to get on the ICO gravy train.

A situation where an ICO is the first money into the company is (likely to be) a thing of the (recent) past. This isn’t necessarily a bad thing: history shows that idea-stage startups which get over-funded rarely succeed. A new technology stack isn’t likely to change that.

The value of the token shouldn’t actually be about how much money you can raise early, it should be about the value flow and creation that you get once there’s a live network. The pre-product token sales actually introduce an existential risk for many of these companies. In cases where the price skyrockets pre-product, the level of value you need to deliver before launch goes up as well. As a founder, you actually don’t want that.

There are a few takeaways here: Token-networks have distinct advantages for venture creation; going public via ICO has both business model and a funding advantage but it’s become expensive to do and conflicts with the way the regulators want to protect the public.

It’s important to note the positive aspect of the SEC DAO investigative report: in a fully distributed token-network where token-holders could organize and self-govern in how their funds get used, there shouldn’t be a principal/agent problem and hence no need for a centralized authority (SEC) involvement. Alas, a fully distributed governance system directly conflicts with a key challenge of the early buildout phase of a product, where a company actually benefits from centralized rather than distributed management. Linux has Linus, Facebook has Mark, Ethereum has Vitalik, Bitcoin had Satoshi. One could ask whether Uber could have been as successful as it became had Travis not led it.

Interestingly, DARPA, the force behind of the Internet, self-driving cars and many of the other technological innovations of today, has a model we can learn from.

DARPA wanted to avoid “kingdom builders” that try to cling to their seat after solving the challenge they were brought on to tackle. DARPA forces a scope and sets a time-capped duration for program managers who lead the different projects.

Program managers know that whatever they do, irrespective of how successful it is, they won’t get to keep their project. Their expiration date is printed prominently on their ID badges, a constant reminder to them and their colleagues that time to accomplish important work is limited. As far as they are concerned, the project “dissolves.” Open Source projects almost unequivocally had a stage where there were a specific initiator and contributor, and “tipped” at one point to becoming community managed.

What if companies were created with a clear charter of building a specific network, with a given timeframe, after which there is an orderly transfer of power?

This is the idea behind the self-destructing company.

Ultimately, this would effectively split the life of a company to reflect three phases: First, we begin with Network Build-out, where a company serves as a “network instigator.” It can be led by a strong founder and raise funding from any accredited source — venture capital or crypto-wealthy individuals — in any format: equity, convertible notes like SAFE, or a promise of future tokens like SAFT. Next we enter Token/Equity Co-existence.

It begins with initial trials of the token economy. During this time the founders build the network with tokens being air-dropped for free or against a deposit (creating vested value for the “depositors” but without regulatory burden as they aren’t actually purchasing tokens) to the actual early customers of the product. This allows the company not to suffer through the regulatory overhead, making its first baby steps as a self-governing entity that gets to decide on its future. Finally, a company goes Token-only at a predetermined point-in-time or milestone when there is a shift of power with the centralized company being “time-bombed” or dissolved away via an ICO. Interestingly, what this means is that ICOs could represent an alternative to later-stage funding, instead of IPOs.

Having the final token-only phase avoids putting the venture management in conflict as to what do they maximize: is it shareholder value or token value? Having a hybrid model during the coexistence phase means you have hybrid, sometimes conflicting, interests.

Mechanics for the disintegration of a company could take a few forms. One possibility is that at the point of the ICO, there is a shares-to-token-swap: equity holders could receive tokens as a dividend in consideration for their shares. A potentially more tax-efficient alternative would allow equity holders to be offered to buy tokens at a variable discount rate that depends on their respective ownership of equity on the cap table. Understanding and planning for this event is important to do before creating the token smart contract, as a shares-to-token-swap could require these additional tokens to be reserved ahead.

This alternative venture-building format offers a few advantages over the traditional company structure that hasn’t changed much since it was developed hundreds of years ago:

-

Initial funding for the projects isn’t dependent on offering tokens to the public and thus doesn’t require significant regulatory oversight.

-

It removes the conflict between maximizing share-holder & token-holder value by having only one asset type for the management to maximize the value of at any given point in time.

-

The founder-led company backed by VC equity will enable companies grow to network maturity, allowing the network to ICO when it’s in a situation that it can comply with SEC regulation and self-governance.

-

In the winner-takes-all world of networks, as it shifts to a token-only structure, the time-bombed company provides a financial incentive to the token holders to create a network effect and grow the network through word of mouth & virality.

The Self-Destructing Company structure is a win-win for future network business models and a fascinating way to bolt new turbo-charged token engines on to old mechanisms of company creation.

Featured Image: Comprehensive Nuclear Test-Ban Treaty Organization/Flickr UNDER A CC BY 2.0 LICENSE