Understanding Roku’s IPO and its growing platform revenues

![]()

In a pleasant Friday surprise, Roku dropped its S-1 document today, detailing its financial performance and corporate strategy.

The filing indicates that the company intends to raise $100 million in its debut. The figure is a widely-recognized placeholder number. The company could raise more or less in its IPO.

Follow Crunchbase News on Twitter & Facebook

As a private company, Roku raised more than $200 million.

The firm, whose IPO was widely anticipated at a valuation around $1 billion, is set to test the market’s waters when indices trade near record highs, video reigns supreme in the media landscape, and some tech offerings have done well. Others have struggled.

Before the weekend impends, let’s slice through how Roku makes money, how much money it makes, and what to make of it all.

How Roku Makes Money

Roku sells TV-focused streaming hardware to consumers, and it also works with content players to get their material in front of consumers. It also has an ad business. The latter two efforts fall under what Roku calls “platform revenue.”

The company’s mix of top-line sources is described in its S-1 in the following fashion:

We generate player revenue from the sale of streaming players and platform revenue primarily from advertising and subscription revenue share on our platform. We earn platform revenue as users engage with content on our platform and we intend to continue to grow platform revenue by monetizing our TV streaming platform.

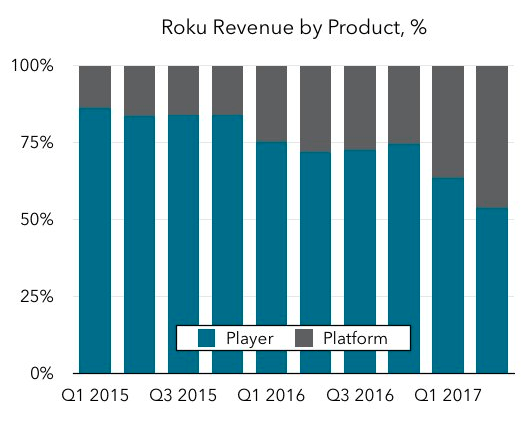

Over time, Roku has increased the percent of its total revenue that comes from its platform business. In practice, it looks like this (via Jan Dawson of Jackdaw Research):

As we’ll see shortly, the mix shift in Roku’s revenue matters as one of the two sources has a far higher gross margin.

Driving the change, it seems, is that Roku drives more usage of its streaming service through partnered-hardware (TVs that run its software) instead of selling hardware over time. This means it can still drive new, active users and engaged hours while not being beholden to selling low-margin hardware.:

So Roku sells hardware for its streaming service, partners with TV manufacturers to sell Rock-powered hardware, drives revenue from partnered streaming companies, and sells ads.

Simple enough, really. How big is Roku? Let’s find out.

How Much Money Roku Makes Loses

Before we dive into the guts of the company, here are the big numbers.

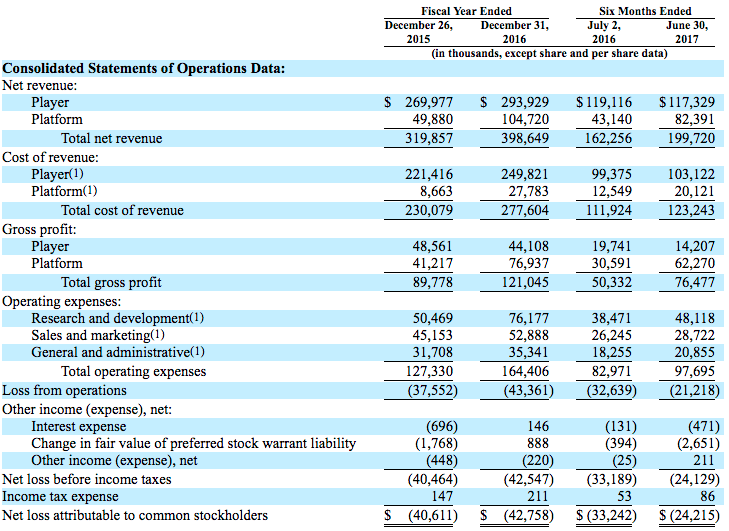

The following chart from Roku’s S-1 shows its 2016 and 2015 fiscal years, and the results of the first half of 2017 compared to the first half of 2016 (calendar). Bear in mind that everything is in units of thousands, so a result of “$119,116” means $119,116,000. Let’s go:

The company’s revenue is expanding while its net losses fall thus far in 2017. The firm’s growth in the 2017 fiscal year came with slightly increased losses.

Roku grew 23 percent in the first two quarters of calendar 2017 compared to the year-ago period. That’s partially due to the company changing up how it brings in revenue. As such, the soft 23 percent figure is more nuanced than it might seem.

Mix Shift

The above-mentioned revenue mix shift makes Roku’s revenue a bit harder to track than it otherwise might be. The firm posted sequential-quarter declines in hardware sales, for example, from the first quarter of this to the second. And, in the second quarter, the firm also posted year-over-year declines in hardware income.

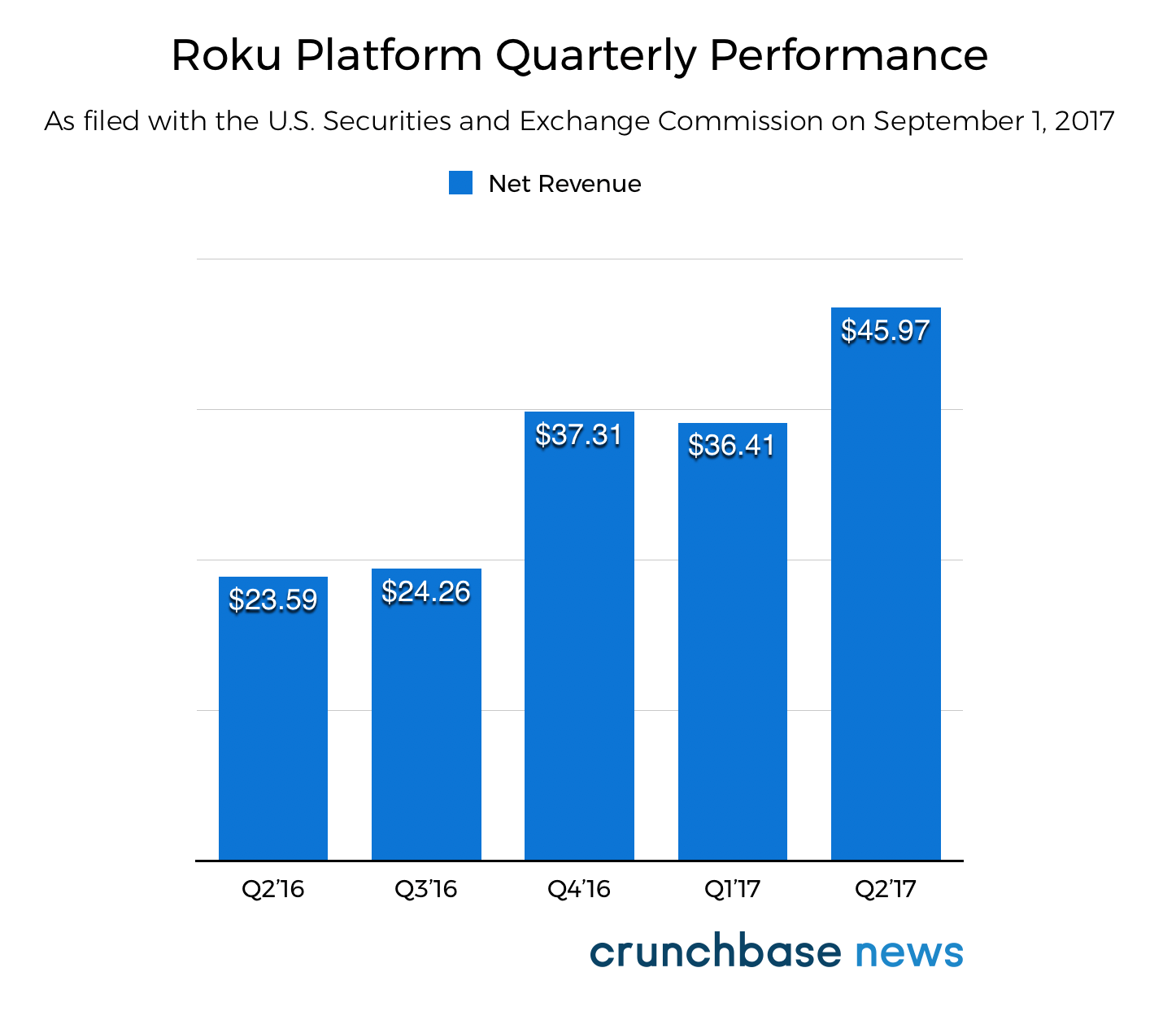

Suffice it to say that the company’s hardware business is in decline. Its platform revenue has grown consistently, however. Going back a few quarters (calendar), here are its results:

As you can see, that is steady revenue growth from Roku’s platform business, aside from the slight Q4 to Q1 dip. Holiday quarters for companies that sell advertisements often see a decline in certain incomes after the close of the holiday-focused fourth quarter. The decline for Roku was modest and quickly offset by growth in the second quarter.

How investors will read that remains to be seen, but the firm has shown dramatic growth of its platform revenue—nearly 100 percent year-over-year.

More broadly, in the quarter ending June 30, 2017, Roku put up $99.62 million in revenue, less than its $100.09 million derived from its first quarter and under its fourth quarter result of $147.34 million. The company, despite its sequential-quarter declines, grew compared to its year-ago periods in each of the last four quarters.

If investors are willing to give more credence to Roku’s growing platform incomes as indicative of its corporate future, the sequential declines may not matter.

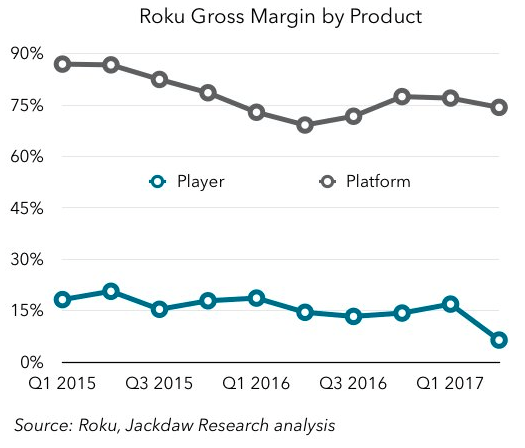

And why might investors care a bit more about Roku’s platform revenue than its hardware incomes? Because the company generates the vast bulk of its gross margin from its platform revenue. Turning once again to Dawson of Jackdaw, the following chart shows precisely how the platform business is more gross profit than the hardware business for Roku:

That’s sharp. What should we make of the above?

What To Make Of Roku’s Finances

Roku must want out of the hardware business, at least as a leading revenue driver. It makes no money in that game. Notably, that makes it in a future-sense a nearly all-in OTT service that doesn’t generate its own content.

That isn’t a model that I would not have thought possible given the incredibly stiff arena of competition for content on the Internet today. Facebook is getting into a game that Netflix is pouring cash into, Amazon is playing, Apple is tinkering in the space, and Microsoft already picked up and dropped its video efforts.

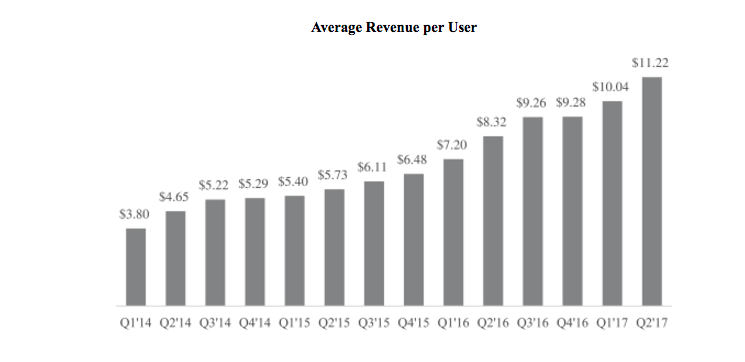

I wonder if that fact might help Roku. It has distribution and content providers want access to audiences. That confluence could be, in part, why Roku’s ARPU is doing this:

That bodes well for the firm that, as we saw before, has a history of active user accretion. Quickly growing high-margin businesses are worth something after all.

What Roku is worth, however, is beyond me. With one revenue stream in decline, persistent losses, but big potential, the firm is going to be a fun one to price.

Hit up the S-1 for more, and send in your best finds.